Published on 14-01-2021

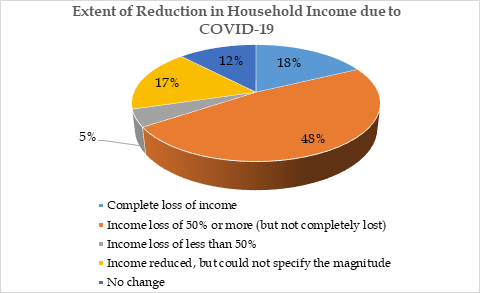

A study conducted by the Centre for Socio-economic and Environmental Studies (CSES), Kochi finds that due to the spread of COVID-19 two-thirds of the rural poor households in Kerala faced an income loss of 50 per cent or more (including the 18 per cent of households who reported a complete loss of income).

Change in Employment Status

The study observes that, following the spread of the COVID-19, almost three-fourths of adults, in the sample households, employed in the pre-lockdown period, either lost their job or experienced a reduction in work (leading to an income loss).

Given the volatile employment scenario, it is necessary to make Mahatama Gandhi National Rural Employment Guarantee Act (MGNREGA) adaptable to crises such as the current pandemic. While it is true that MGNREGA is currently operational, several factors limit its scope in the COVID-19 situation. Firstly, there is an exclusion in the participation of those above 65 years in the MGNREGA. For Kerala, with a high share of the elderly population, limiting participation in MGNREGA to those below 65 plus age would exclude a significant share of desperate job seekers. Secondly, given the pandemic situation, there should be an effort to include new forms of work under the purview of MGNRGEA; something which could use the labour of elderly in a safe environment, say the making of face masks, sanitiser, for example. Thirdly, there should be an effort to strengthen the implementation of MGNREGA, by not putting a ceiling on 100 days of work. It is also important to identify works suitable to be taken up in the MGNREGA and provide eligible job seekers employment opportunities. Guidelines for implementing MGNREGA should be reviewed to make the programme adaptable during any similar future crisis. Remodelling the scheme by introducing more flexibility in the work choices, number of working days and wage disbursals may help economically vulnerable sections withstand crisis when they face reduced work opportunities and income loss.

Study also observes the need to relook at the options available at the local level to enhance household income. The local government shall devise innovative schemes to boost employment and entrepreneurship at local level in partnership with Kudumbashree and co-operative institutions. Efforts should also be made to learn and adapt successful models, Palliayakkal Service Co-operative Bank Ltd, to promote the local economy.

Indebtedness

Following the COVID-19 outbreak, 72 per cent of the sample households borrowed during the period to withstand the jobless-income less situation. The average amount of additional debt burden created by the rural poor households since the beginning of lockdown is Rs. 40,667. Kudumbashree and friends and relatives emerged as the majorly depended credit sources by rural poor households during the current pandemic.

| Type of Credit Sources | Proportion of Households |

| Kudumbashree | 57.2 |

| Friends & relatives | 39.2 |

| Primary Cooperatives | 22.9 |

| Moneylenders | 12.0 |

| Commercial banks | 10.8 |

| NBFCs | 9.6 |

| Private MFI | 5.4 |

| District Cooperative Banks | 3.0 |

| Other self-help groups | 3.0 |

Kudumbashree served as a crisis management mechanism during the present crisis. The COVID specific interest-free loan distributed through Kudumbashree (Chief Minister’s Helping Hand Loan Scheme) helped many to withstand the pandemic. However, 30 per cent of the rural poor households are still outside the Kudumbashree network, depriving them of an easily accessible source of credit and other benefits; making them more prone to a financial shock. This disparity was reflected in the credit source choices of rural poor households with and without Kudumbashree membership. The study noted high reliance on money lenders, friends and relatives among families who do not have Kudubmbashree membership compared to those with Kudumbashree membership. The government should take urgent measures to identify and bring vulnerable households into Kudumbashree to enhance social protection.

A notable point that emerges from the study is that, even on the wake of a financial breakdown, 30 per cent of the sample households took loan only for debt servicing. Responses from the survey and interviews held with the bank officials and Kudumbashree authorities indicate that Reserve Bank’s moratorium did not provide relief to those in distress to the extent envisaged. Two main reasons could explain the situation; firstly, confusion over the nature of moratorium—whether it is mandatory or discretionary; secondly, the non-waiver of interest amount during the moratorium period. Several cases of financial institutions not allowing moratorium and pressurising households to repay their loans were noted. Bringing clarity to RBI guidelines on the moratorium, stating stipulation on private financiers to their customers in explicit terms should be made. Facilitating information flow on the moratorium at the local level and providing checks and balances to protect rural households from the harassment of financial institutions would be effective measures to provide relief to rural poor households who are in distress due to the pandemic.

For more details contact

Aswathi Rebecca Asok

Ph: 9958525385/8075095152

E-Mail: aswathirasok@gmail.com